EU Omnibus announcement: key changes to corporate sustainability reporting

On February 26, 2025, the European Commission unveiled the Omnibus package, a series of proposals aimed at simplifying EU ESG regulations to enhance business competitiveness. A significant aspect of this package involves modifications to the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD), which have substantial implications for businesses across Europe.

What are the Key Proposed Changes?

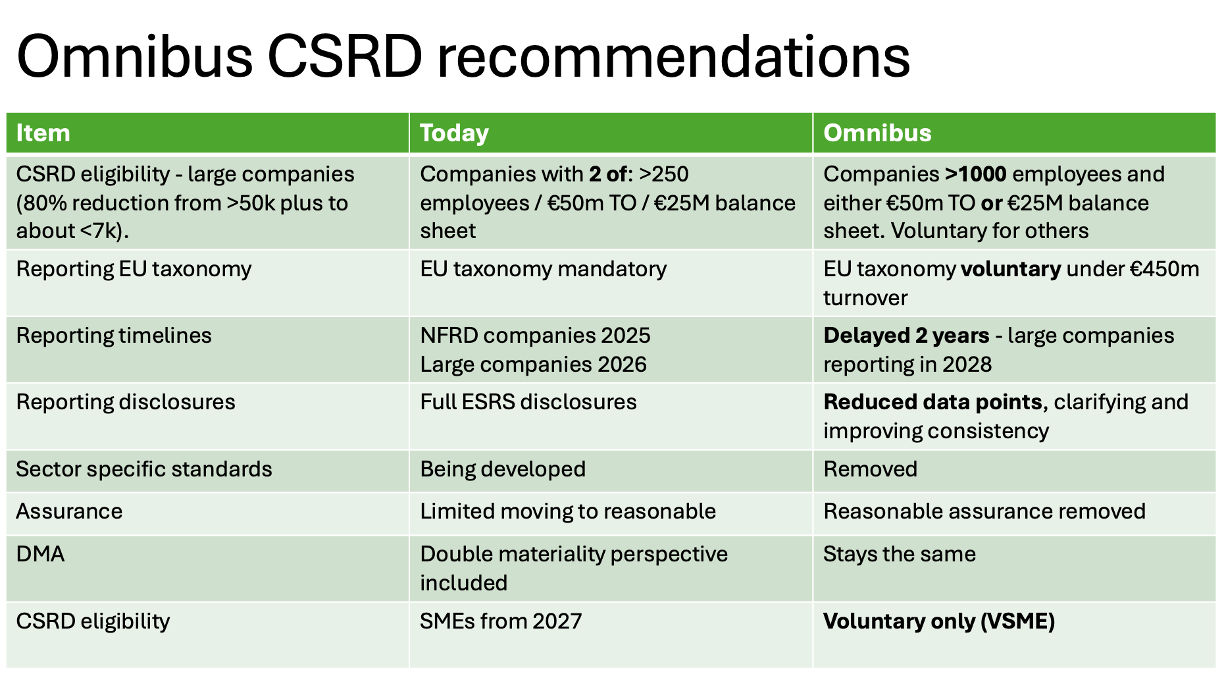

- Fewer companies required to report – from >50,000 to <7,000.

- Voluntary standards launched for those companies not obliged to report.

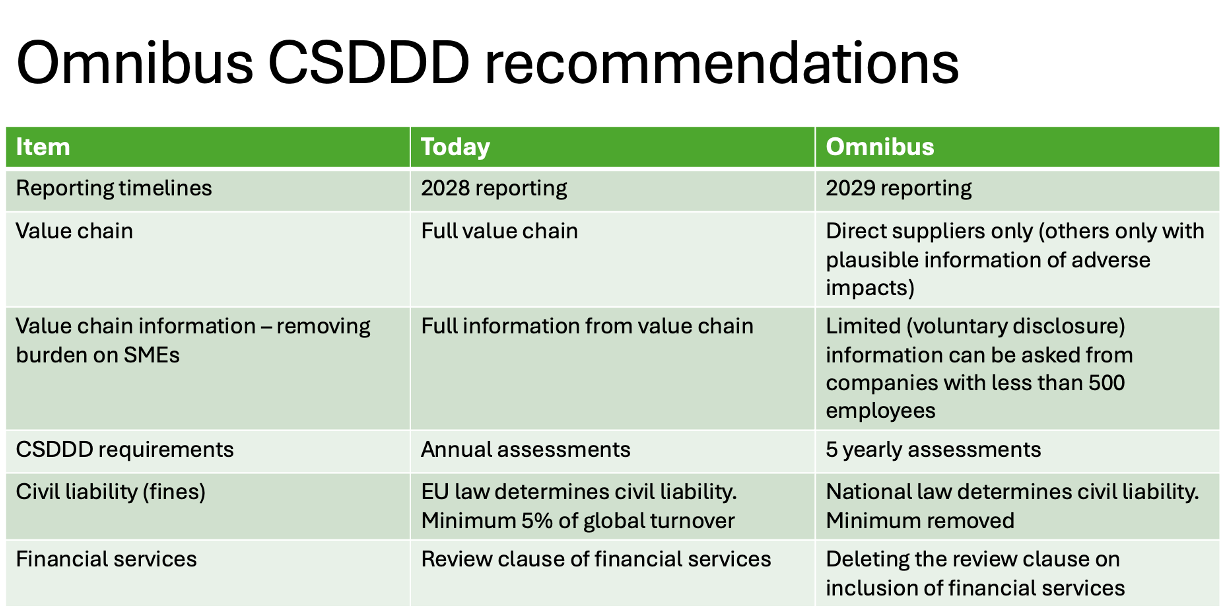

- Due diligence limited to direct suppliers, removing indirect supplier obligations.

- Sector-specific sustainability standards no longer being developed.

- Mandatory minimum 5% penalties for non-compliance scrapped and new guidance being drawn up.

These changes aim to reduce corporate red tape but raise serious concerns for climate and environmental goals.

What changes for CSRD?

The proposed changes focus on narrowing the scope of companies required to comply with CSRD reporting obligations:

- Reporting Requirements Shrink

- Thresholds rise to >1,000 employees (previously 250+) and either €50m turnover or €25m in assets.

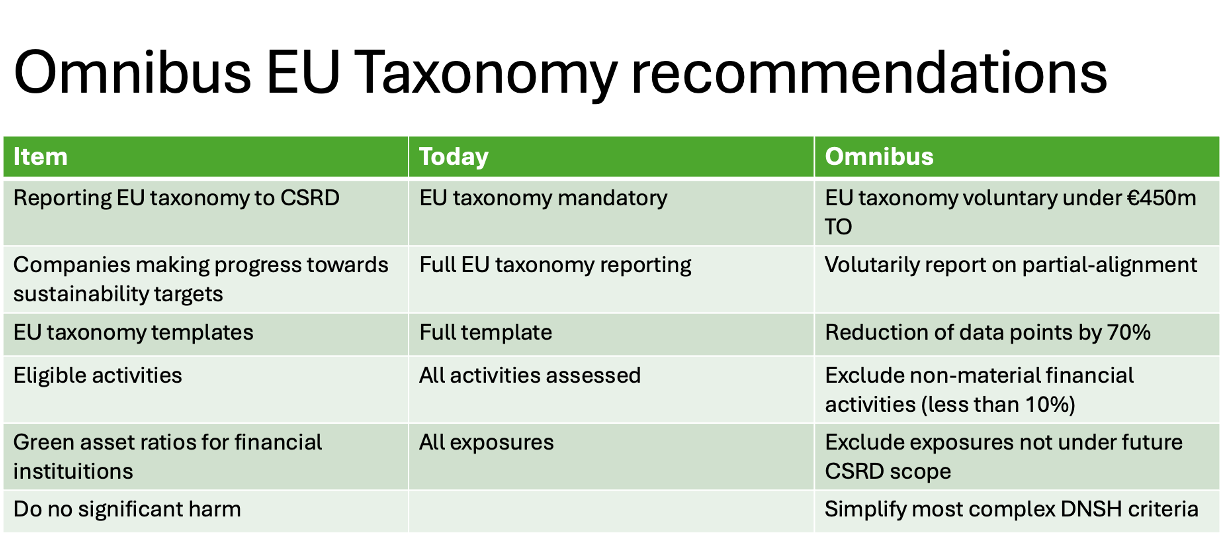

- Non-EU companies threshold rises from €150m to €450m turnover

- Data collections from non-CSRD suppliers should be limited to voluntary standards data.

- Sector-specific standards no longer being developed, reducing comparability.

- Deadlines to be delayed by two years.

The table below outlines the current versus proposed parameters for CSRD, CSDDD and EU Taxonomy:

What does this mean for ESG and sustainability in business?

The key impact for sustainability in the EU

- The changes potentially remove around 80% of companies from the scope of CSRD, focusing the sustainability reporting obligations on the largest companies which are more likely to have the biggest impacts on people and the environment

- It would ensure that sustainability reporting requirements on large companies do not burden smaller companies in their value chains

- The Commission has a clear target to deliver an unprecedented simplification effort, by achieving at least 25% reduction in administrative burdens, and at least 35% for SMEs until the end of this mandate

- It would also postpone by two years (until 2028) the reporting requirements for companies currently in the scope of wave 2 & 3 of CSRD, which are required to report as of 2026 or 2027.

- If adopted and implemented as set out today, the proposals are conservatively estimated to bring total savings in annual administrative costs of around €6.3 billion and to mobilise additional public and private investment capacity of €50 billion to support policy priorities

The full EU Omnibus proposal is found here with the Q&A also linked in this article: https://commission.europa.eu/news/commission-proposes-cut-red-tape-and-simplify-business-environment-2025-02-26_en

What does this mean for your business?

Whilst the Omnibus was released this week (26 February 2025), nothing changes overnight. Businesses may be tempted to alter their course, believing that everything is changing, but that is not the case. Business actions should be determined by overall strategy to date and the primary motivations behind that strategy. Let’s consider some key factors:

Timing is critical

The CSRD has already been been passed in national laws in many EU countries, so companies are currently legally required to comply with CSRD. There is no suggestion of suspension or pause in these obligations yet as this is a proposal, while the EU are aiming to push this through and the delay is potentially the first part of the legislation that will be ratified.

The EU Omnibus proposal will need to pass 6 formal steps of review and approval as part of any EU legislative process. The announcement this week is only step 1 of the process. If it follows recent legislative timelines, it could easily be several years before it is fully enacted, though the EU wants to push through the delay as soon as possible and the rest of the legislation is proposed to be streamlined, avoiding all going through all the usual process.

Reporting for ‘so called Wave 2’ companies proposes to be delayed until 2028, which means the Omnibus delay would need to be passed into law within the next 10 months, for that deadline to change anything for Wave 2 companies in the short-term. By comparison, it took the Commission 25 months to deliver the full CSRD in to law. The delay is proposed to go through on an accelerated timeline meaning that this is more likely to be achievable.

So, companies that choose to pause or delay their CSRD preparations in anticipation of the Omnibus changes would be taking a risk. If the proposed delay is not made law by December 2025, Wave 2 companies would still need to report by January 2026.

However, there is an opportunity to adjust the focus of the ongoing work to gain the maximum benefits from CSRD rather than purely focusing on compliance.

Remember the true value of CSRD

Many companies understand that CSRD is a strategic tool, some even choosing to comply voluntarily, seeing CSRD as a gold standard in sustainability reporting – such is the respect and value for the ESRS framework.

For example, currently mandatory under CSRD, double materiality assessments are crucial for long-term sustainability and strategic ESG planning, irrespective of legislative compliance.

It is widely believed that few other frameworks offer the same strategic insight. With or without the demand for legislative compliance, employing CSRD gives all businesses a methodology to future-proof, focusing on value chain analysis, impacts, risks and opportunities, policies, actions, metrics, and targets.

If implemented, the Omnibus ultimately simplifies and streamlines this opportunity. It eases the path for businesses already on course to CSRD. And for all businesses, this lower cost of entry, including the possibility to use to new voluntary standards, enables a step up to a framework previously seen as prohibitively demanding.

In conclusion

Ikano Insight has long focused on the benefits of CSRD to business, and it is our view these benefits may become more accessible for organisations if Omnibus proposals are implemented.

The potential risks and impacts of climate change, social disruptions and governance challenges will not reduce anytime soon, irrespective of legislation. On the flip side there are many opportunities from looking after the environment and people. The case for ESG framework implementation in any business is strong, and the Omnibus announcement should not divert the strategies of organisations.

Written by Peter Jones

Head of Sustainability

Skilled in sustainability strategy and analytics, Peter is passionate about steering organisations toward a sustainable future, leveraging strategic vision and extensive experience for global betterment and bottom-line success.